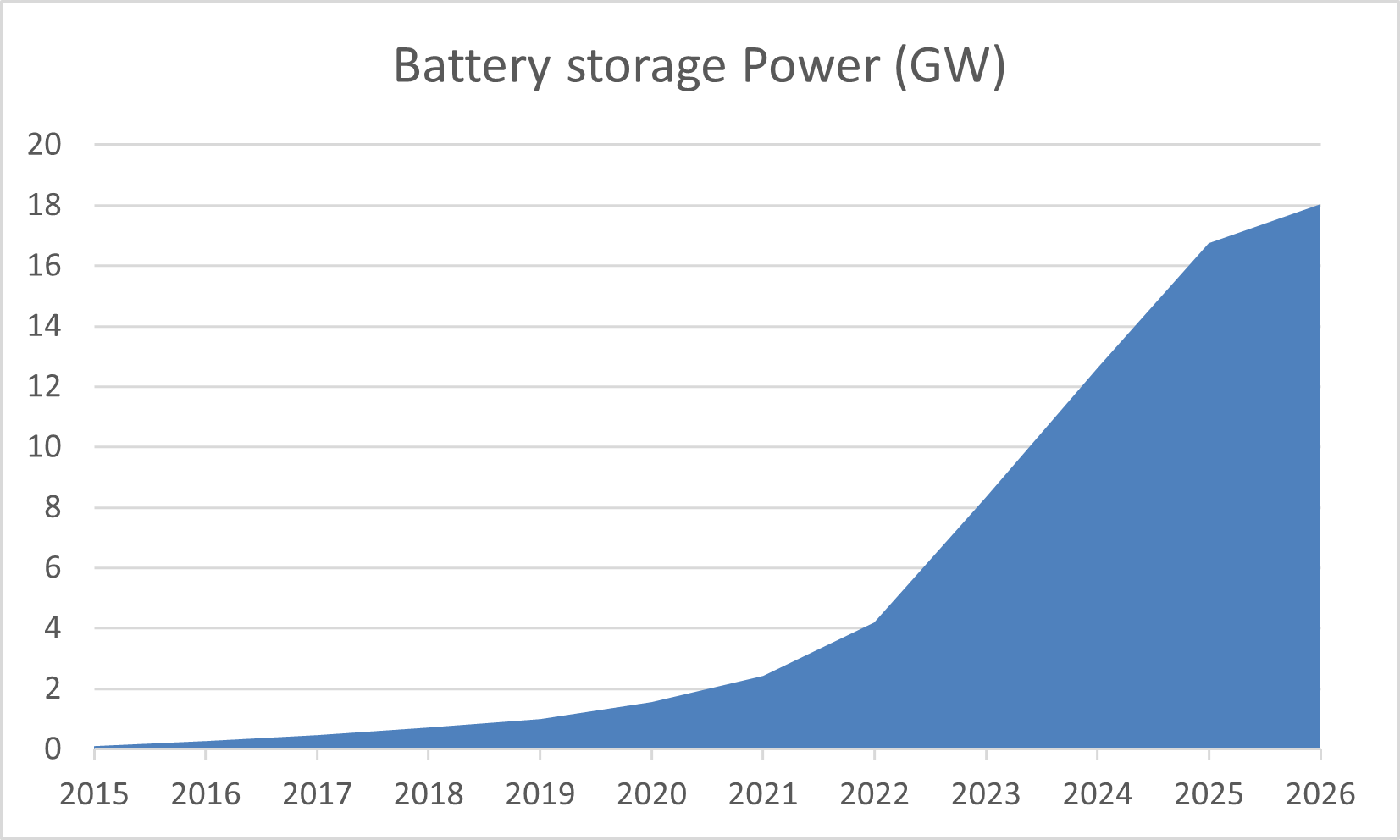

Strategic Outlook 2026: The Maturity of the European BESS Market

The landscape for large-scale battery energy storage systems (BESS) in Europe is undergoing a fundamental shift. We are moving from a phase of early, opportunistic growth into a more complex and operationally mature era. For developers, investors, and grid operators, the priorities have changed: it is no longer just about proving the concept, but about mastering the technical and regulatory nuances that define long-term project success.

Based on current market developments and industry consensus, several key themes are defining the BESS sector in 2026.

1. Fundamentals remain strong – but execution is the new differentiator

There is a broad consensus across the financial and energy sectors that battery storage is the backbone of Europe’s energy transition. As critical infrastructure, batteries provide the necessary flexibility and stability for a renewable-heavy grid.

However, the "easy wins" are largely gone. Today’s challenges have shifted from "why storage?" to "how to execute?". Tighter scrutiny from lenders and stakeholders means that success is now measured by:

- Precise grid-connection strategies

- Bankability of multi-stacked revenue streams

- Sophisticated risk allocation between all project parties

2. Grid connection as the dominant constraint

Access to the grid has overtaken land and capital as the scarcest resource in the industry, particularly in markets like Germany.

Current market observations:

- Grid capacity is the primary bottleneck for new deployments.

- System operators (DSOs and TSOs) are increasingly turning to Flexible Connection Agreements (FCAs) to manage local congestion.

- The variability in FCA structures creates significant uncertainty, often leading to prolonged negotiation cycles.

For developers, the predictability of operational constraints is now as vital as the availability of the hardware itself.

3. The evolving role of Flexible Connection Agreements (FCAs)

FCAs have moved from a niche requirement to a standard necessity. While they enable quicker connections in congested areas, they remain a double-edged sword.

Current technical challenges include managing ramp-rate limits and restrictions on certain ancillary services. The lack of standardisation across different regions still creates project-specific risks. However, advanced optimisers and traders are proving that these constraints can be managed through smarter, portfolio-level dispatch strategies without undermining bankability.

4. Revenue models: Shifting toward stability

While fully merchant models still exist, the financing landscape has become more conservative regarding pure merchant exposure.

Key market trends:

- Lenders now frequently expect partial revenue stabilisation, such as tolling agreements or "floors".

- Capacity mechanisms (notably in Poland and Italy) are proving highly effective in de-risking projects while still allowing for merchant upside.

- Hybrid contracting – combining fixed-price elements with merchant exposure – has become the preferred structure for balancing risk and return.

5. Co-location and hybrid projects as the new standard

A significant shift is occurring toward co-located PV + storage projects, especially in Central and Southern Europe.

The drivers are clear: better utilisation of existing grid infrastructure and a natural hedge against price cannibalisation. While co-location adds operational complexity – particularly regarding metering and regulatory treatment (e.g., "green vs. grey" charging) – many developers have reached a point where they no longer plan large-scale PV projects without an integrated storage component.

6. Grid-forming capabilities: From theory to practice

Technical requirements are becoming more stringent. Grid-forming batteries and system stability services (like inertia provision) are no longer "nice-to-have" features; they are increasingly mandated by TSOs.

Technical compliance, sophisticated modelling, and depth of certification have become key differentiators for manufacturers and integrators. Those who can prove system stability support are finding themselves at a significant competitive advantage.

7. Performance and longevity under the microscope

As the asset class matures, investors are paying closer attention to the "life-cycle" of the hardware. System availability, degradation assumptions, and long-term service guarantees (LTSAs) are now core components of any due diligence process. Early-stage design decisions and procurement quality are the primary factors determining whether a project remains viable over a 15 to 20 year horizon.

8. The impact of regulatory timing

Regulatory uncertainty continues to be a backdrop for the European market. Critical decisions regarding grid tariff reforms, redispatch rules, and the treatment of storage within existing support schemes are still in flux. In many regions, the pace of investment certainty is still struggling to keep up with high political ambitions.

Conclusion: Mastering the Complexity

The European BESS market in 2026 is no longer about headline growth alone – it is about execution excellence.

Success in this mature phase requires an integrated approach that combines early-stage grid strategy with robust technical design and bankable revenue structures. The competitive advantage now belongs to those who can navigate the operational and regulatory complexity with precision.

One thing is certain: storage is no longer an optional add-on, but the essential infrastructure that makes the carbon-free grid possible.

Guy de Macedo

He is the product manager for mc Assetpilot and mc Cloud at meteocontrol. His responsibilities include assisting customers with the application, including the development of new features.